A Tale of Three Markets: What’s Hot & What’s Not

As we move further into the spring market, we’re starting to see a clearer picture of how 2026 is unfolding and it’s not quite the strong surge many sellers were hoping for.

While activity has picked up from earlier in the year, the market remains more balanced and segmented, with each property type telling a slightly different story. Some areas are gaining momentum, while others continue to face challenges.

📊 March Snapshot – Victoria Real Estate Board Region

• 579 properties sold in March

• ⬇️ 5.5% fewer sales than March 2025

• ⬆️ 24.5% increase over February (spring momentum building)

• 3,261 active listings

• ⬆️ 12.3% more inventory than February

• ⬆️ 7.9% more than last year

This reflects a typical spring pattern, with both sales and listings increasing and activity expected to continue building toward May and June.

💰 Average Sale Prices – March 2026

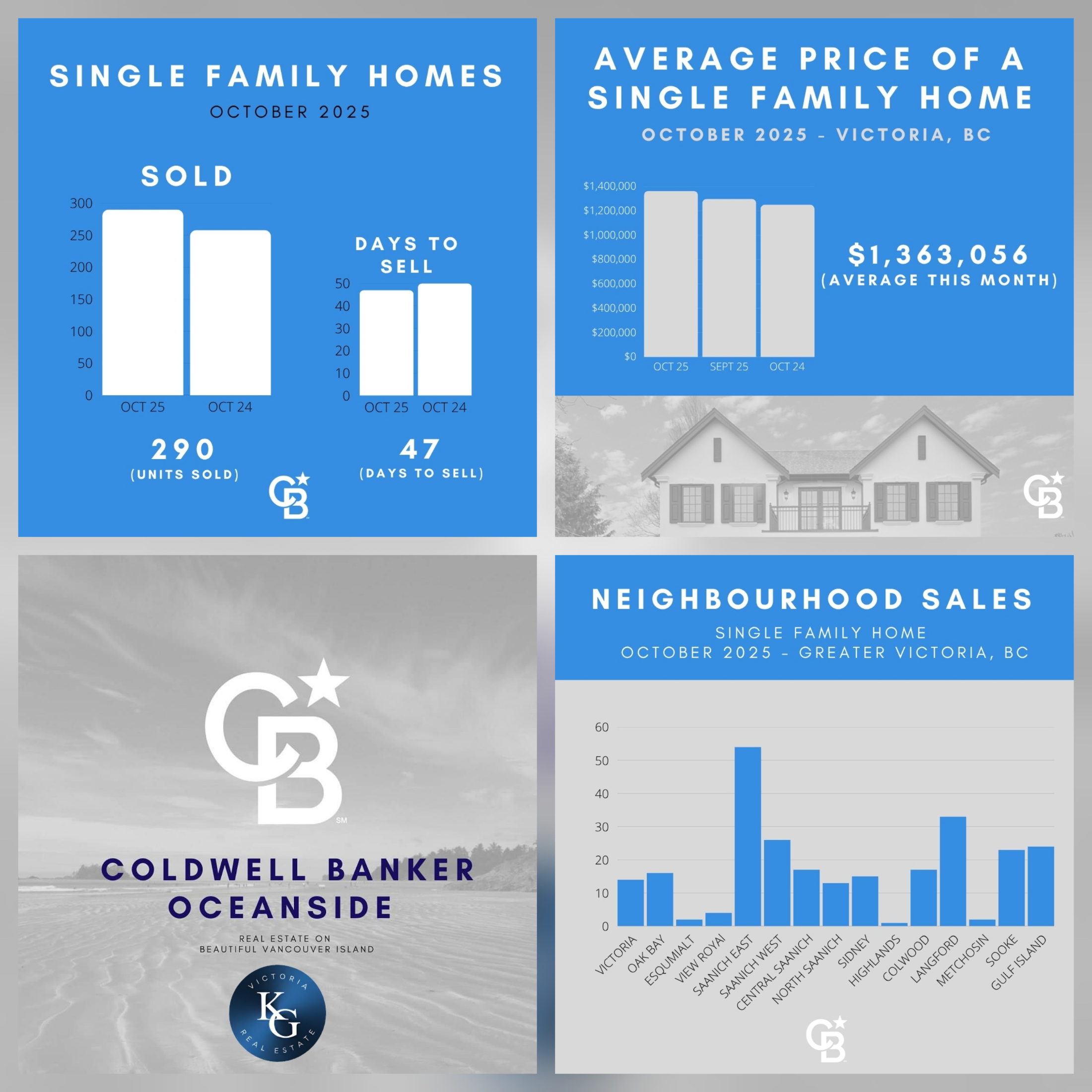

🏡 Single-Family Homes: $1,341,863

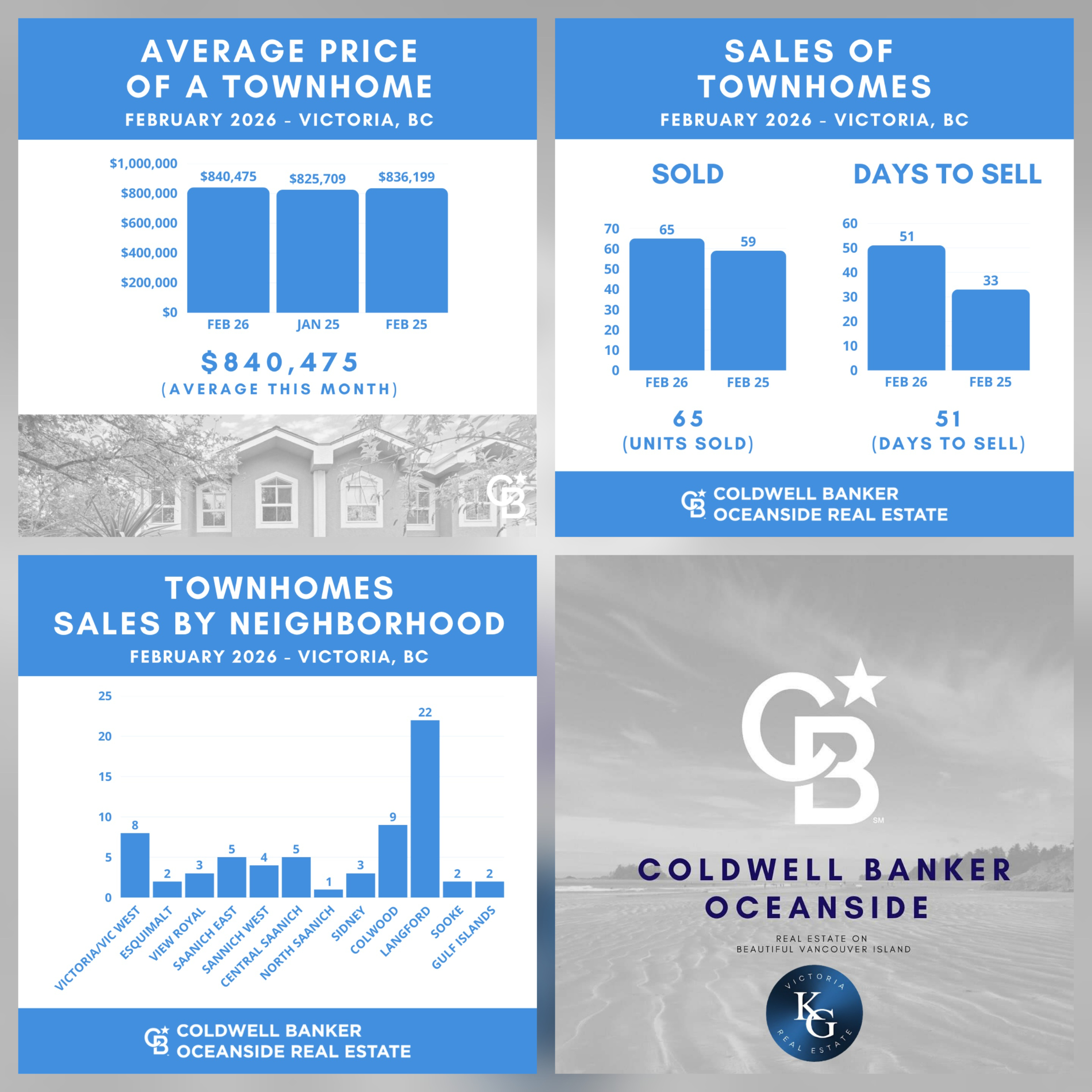

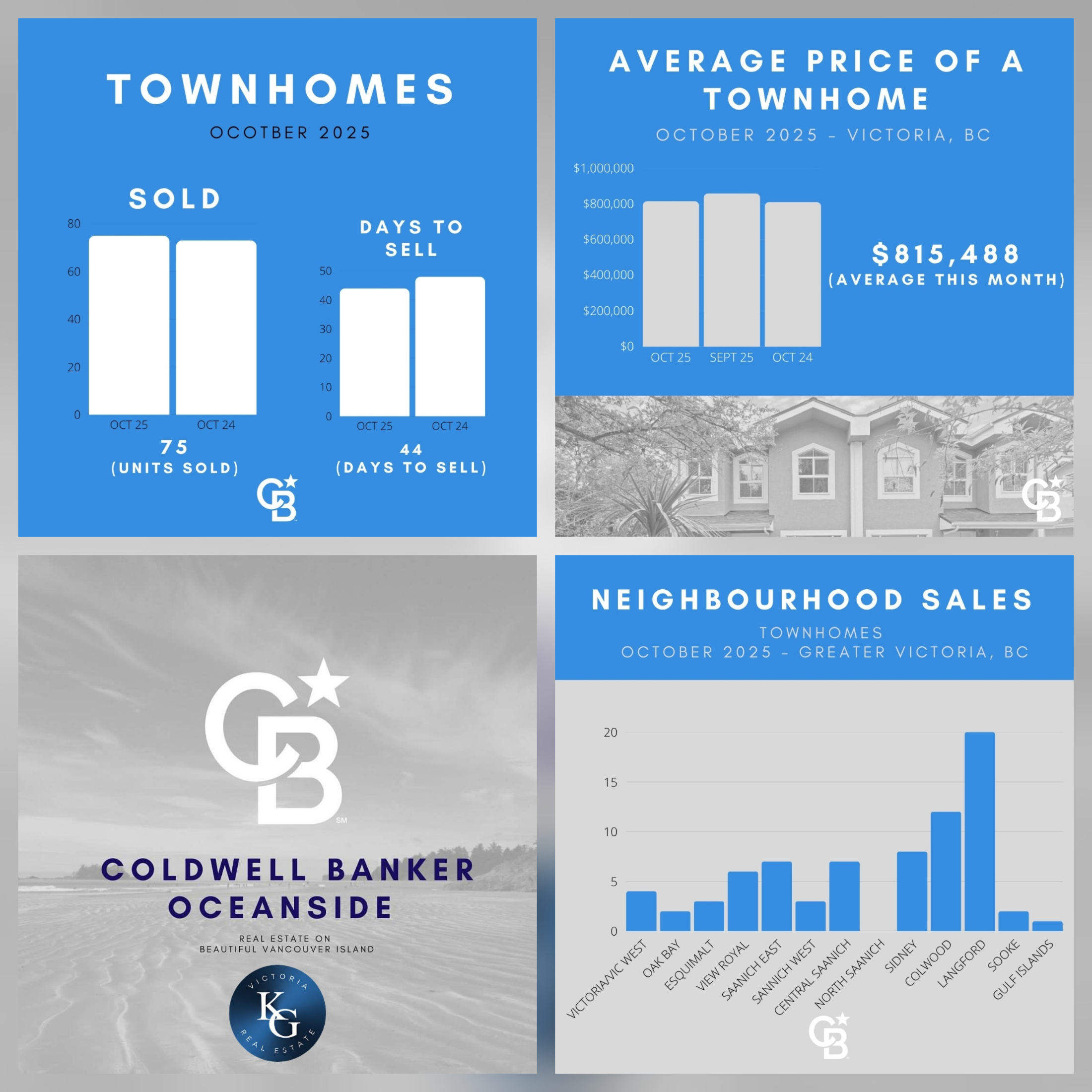

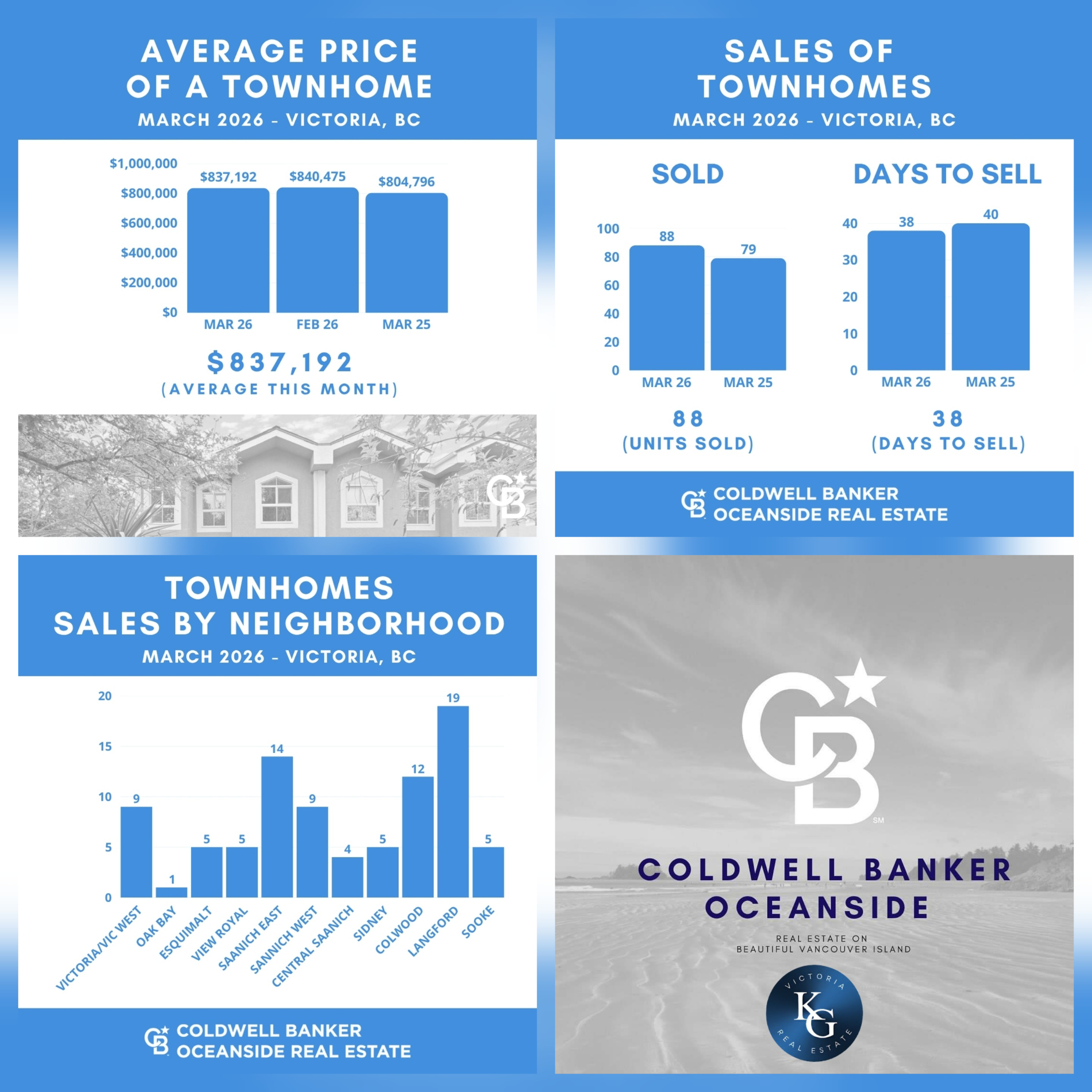

🏘️ Townhomes: $837,192

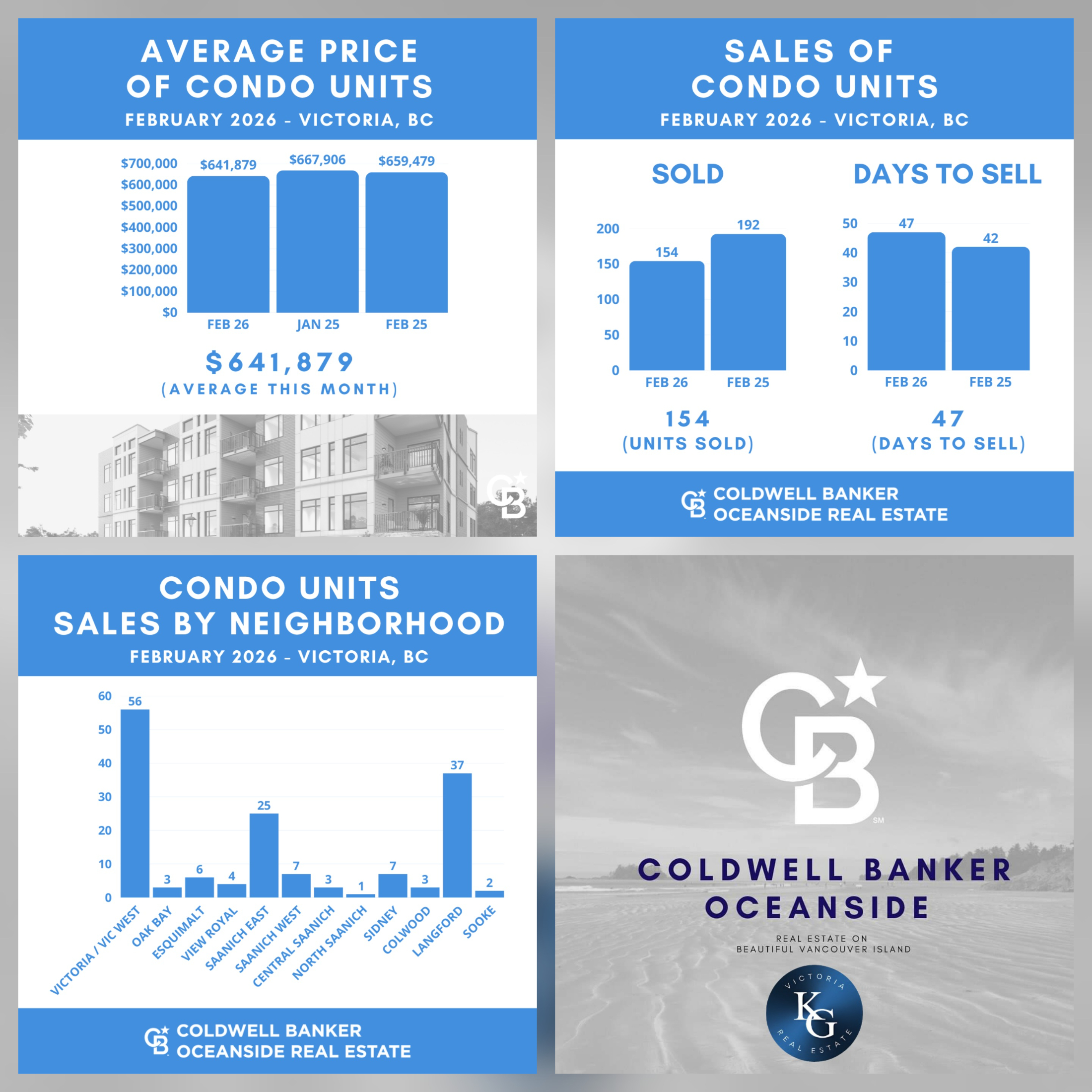

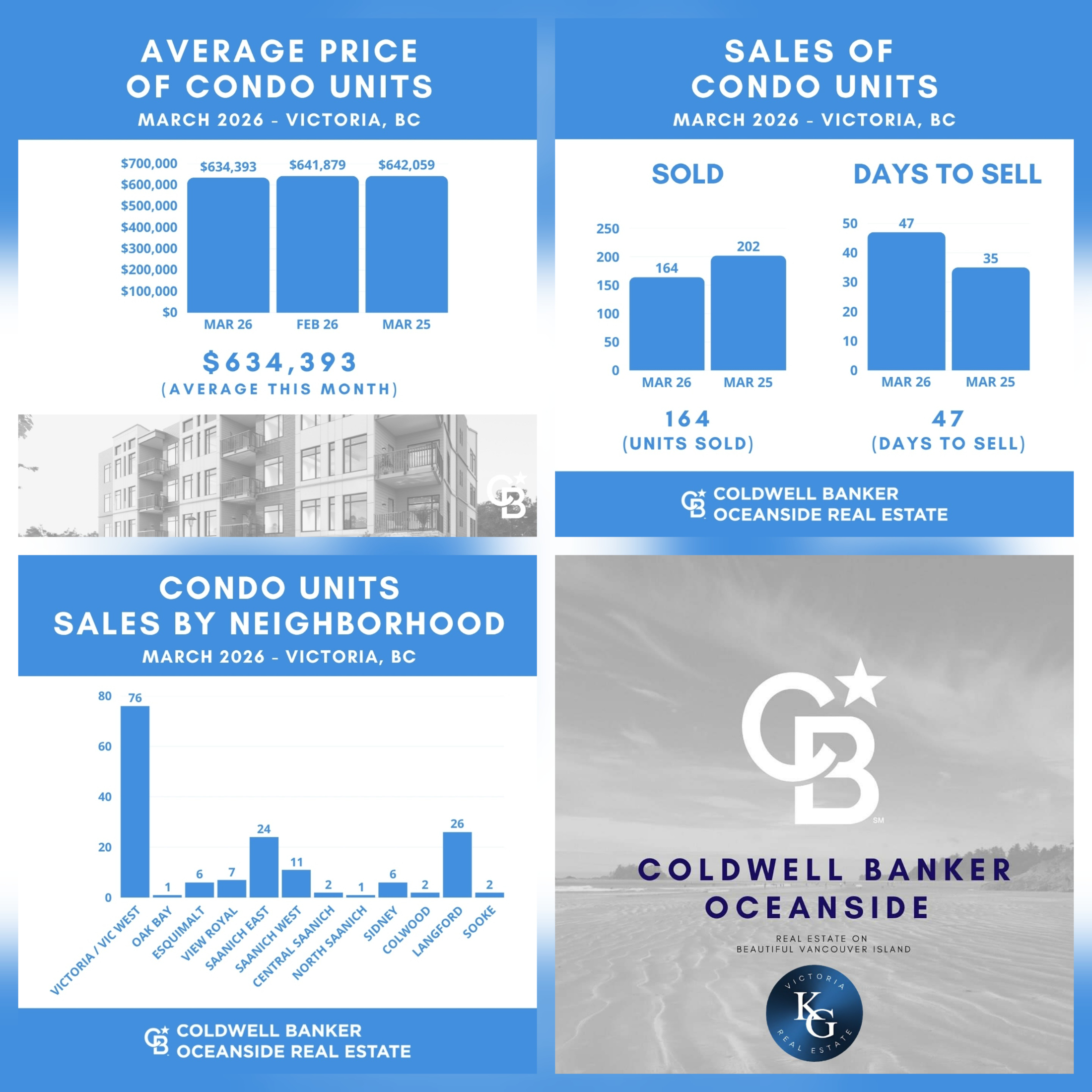

🏢 Condos: $634,393

Prices overall remain relatively stable, even as sales volumes fluctuate, a key theme across all property types.

🏠 A Closer Look at the Market

🏡 Single-Family Homes

After a slower start to the year, this segment is showing clear signs of improvement.

Sales are still slightly below last year, but have rebounded significantly from the early months of 2026. Inventory is now more in line with 2025 levels, and days on market are beginning to shorten.

💡 There is a strong possibility we’ll see increased activity through April and into late spring.

🏢 Condos

The condo market continues to face the most pressure.

Sales remain well below last year and significantly under long-term averages. Despite this, prices have not dropped substantially, which may be contributing to slower sales activity.

💡 Buyers have more choice and negotiating power here, making this one of the most opportunity-rich segments.

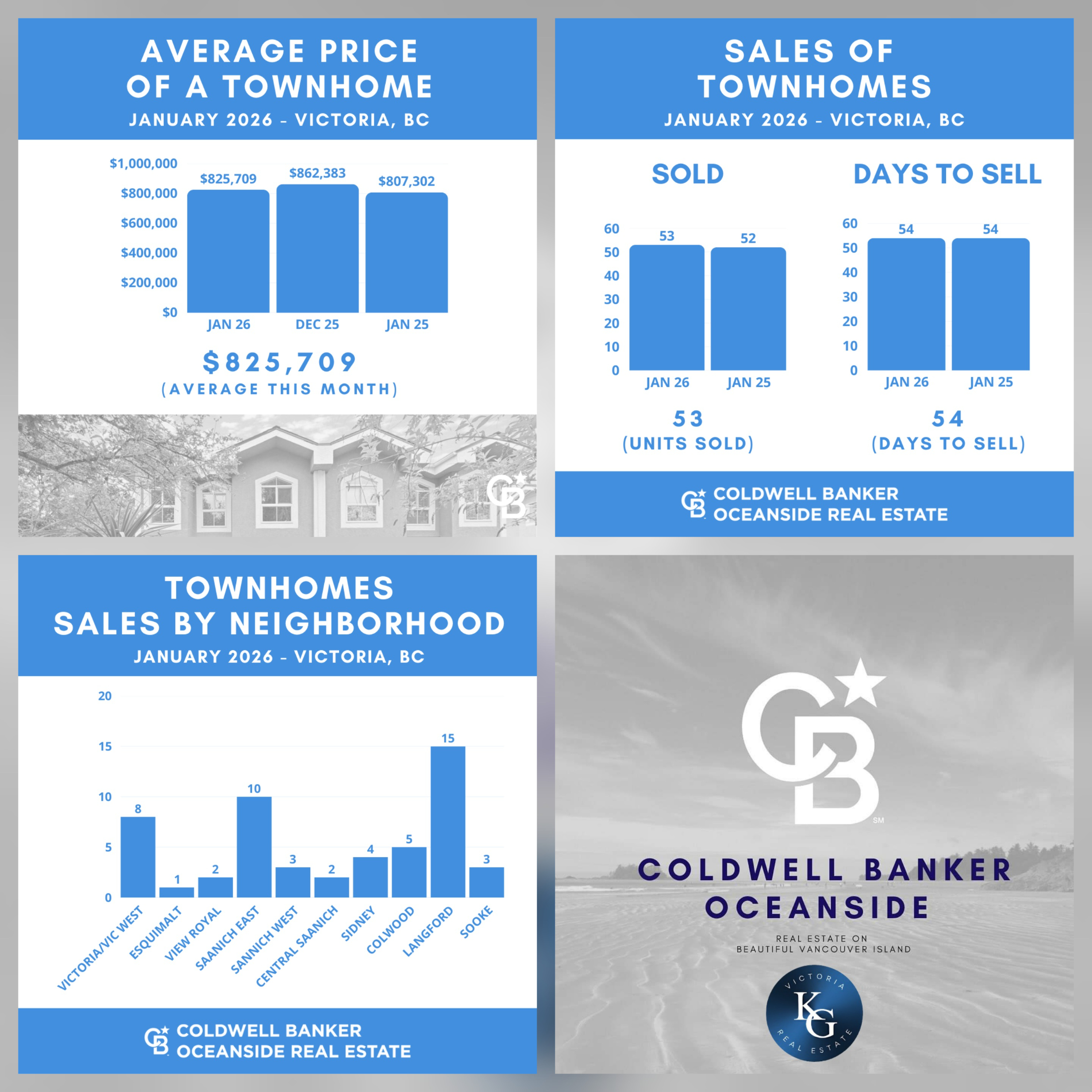

⭐ Townhomes – Leading the Way

Townhomes continue to be the standout performer in today’s market.

Sales are up month-over-month, year-over-year, and above long-term averages.

Even with increasing inventory, demand remains strong, and well-priced townhomes are selling quickly, often very close to asking price.

💡 This remains one of the most competitive and reliable segments for sellers.

⚖️ Risks & Opportunities

This market presents a mix of both, depending on your position.

For Sellers:

✔️ Spring (April–June) is typically your strongest window

✔️ Strategic pricing is critical in today’s inventory-heavy environment

✔️ Well-priced homes stand out — especially against overpriced competition

✔️ In-demand segments (like townhomes) continue to perform very well

For Buyers:

✔️ More inventory = more choice and less pressure

✔️ Strong negotiation opportunities in certain segments (especially condos)

✔️ Best-value properties still move quickly and preparation is key

📈 What to Watch

Interest rates continue to be a major factor. There is increasing discussion around potential rate changes through 2026, which could impact affordability and buyer confidence.

Because of this, many buyers are choosing to act now, securing a property and locking in financing before further changes occur.

🌷 Final Thoughts

The 2026 market is shaping up to be more strategic than reactive. Gone are the days of one-size-fits-all conditions, success now depends heavily on property type, pricing, and timing.

With Greater Victoria made up of many unique micro-markets, having a tailored approach is more important than ever.

If you’re thinking about buying, selling, or simply want to understand how this applies to your specific situation, I’m always happy to help.

📞 250-893-9185

I’ll also include a link below to view full market stats and graphs for a deeper dive.

🔗 Victoria Real Estate Market Update: See the Latest Trends and Stats!